When key people leave a money management firm, it is often cause for concern – particularly when key personnel leave in packs. While one of my older blog posts laid out a framework for dealing with changes in lead managers, it’s also helpful to recognize when change is positive. This can only be confirmed in hindsight but two recent manager changes seemingly bode well for investors going forward.

Internal Shuffle

Last month, TD Asset Management announced the departure of John Smolinski, TD Canadian Equity lead manager since 2001. Given that Smolinski outpaced the S&P/TSX Composite during his tenure, albeit by a small margin (see chart), many might conclude that this was bad news for investors’ $2.5 billion in this fund. Quite the contrary – at least in my opinion.

I had concluded by 2004 that Smolinski’s approach involved much more risk than was apparent in the numbers at that time. The more obvious data points that jumped out included high turnover (almost 250% annually under his tenure) and the resulting trading costs (averaging more than 0.5% annually). But these figures were not my primary worry.

My first awareness of the lead manager was in 1999 when he left Royal Life to join Mackenzie’s Ivy Team. The firm’s purchase of Nortel Networks in late 1999 was probably – in hindsight – influenced by Smolinski. He joined TD Asset Management to lead its Canadian Equity fund in 2001. Within three years, Nortel also showed up in that portfolio. The coincidence was too strong to overlook so I started digging.

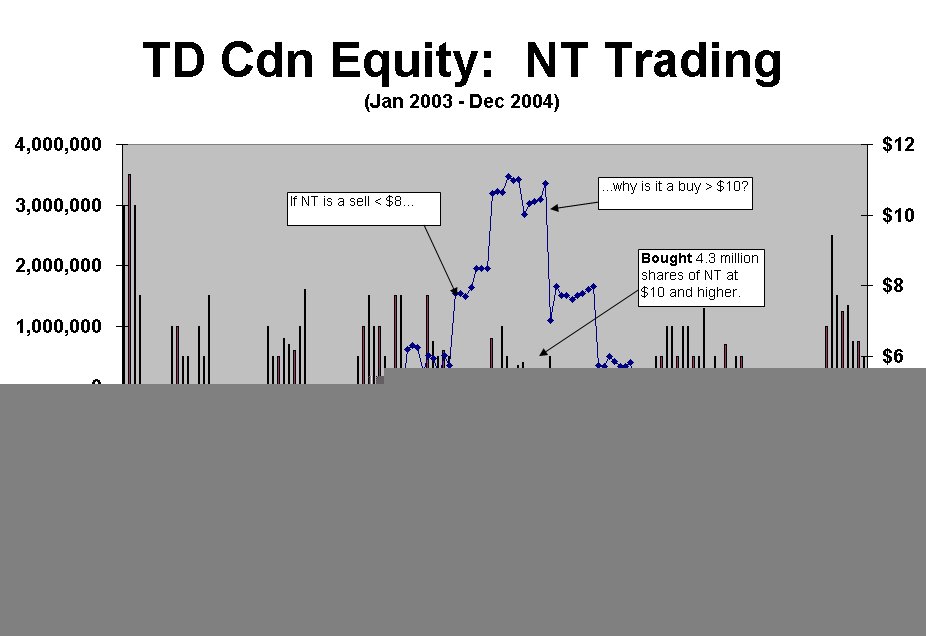

I discovered that the fund had traded in and out of Nortel throughout 2003 and 2004 in a pattern that made no sense to me. I summarized the fund’s Nortel trading in the below chart (click on chart to enlarge). I surmised that the stock’s presence was influenced more by its heavy allocation in the index at the time than its earnings, profits or other fundamentals.

(Note: Prior to 2006, mutual funds were required disclose trading summaries through SEDAR or upon request. Fund companies must track this information internally but unfortunately no longer release such details because regulators no longer require it.)

{kind=link}

Raw data source: TD Canadian Equity mutual fund filings, www.SEDAR.com

TD expects turnover to fall significantly (thereby pulling down embedded trading costs). In a recent presentation they also said that the portfolio will be more focused and probably less volatile. Even though this fund won’t ever be my favourite, it didn’t take long to conclude that the change is likely an improvement for unitholders.

Falling off the wagon

AGF has had its share of missteps when it comes to manager selection but a recent change looks promising for its fund investors. Last month AGF’s Tony Genua replaced Chicago-based momentum manager Driehaus Capital Management on two funds after very a long tenure on each. (This also helps AGF’s bottom line by internalizing management.)

I admit to being among the many who, in the 1990s, occupied a seat on the Driehaus bandwagon. But my view changed about ten years ago. Driehaus claimed to screen for stocks with good earnings and price momentum while buying only those with the ability to sustain this positive momentum. It all made sense to me for a while and it worked for a long time.

By 2003 I had a change of heart, concluding that I had over-estimated the firm’s ability to do meaningful qualitative assessments on portfolios of companies that were routinely turned over more than twice annually.

Driehaus’ U.S. mid-cap and global mid-cap strategies soared during the tech boom but effectively blew up in the bursting of the bubble – losing 74% and 67% respectively by early 2003. Both funds remain far below their 2000 peaks. I put my changed opinion in writing in mid-2003.

Driehaus replacement Tony Genua has been a rare bright spot for the struggling independent fund company. He joined AGF in January 2005 to run its flagship American Growth Fund in 2005. He has kept pace with the tough-to-beat S&P 500 index net of the fund’s near-3% management expense ratio. That’s no small feat, particularly since his AGF tenure came after posting a solid U.S. equity record with his former firm.

Time will confirm whether the above changes are indeed positive for investors. But don’t assume that a change in managers – even on a successful fund – is a negative. Sometimes change is necessary to ensure investors’ future success.

- Piling into U.S. stocks? Don’t Expect the Past Decade to Repeat - January 15, 2025

- The S&P 500’s Three Surprising Traits - November 6, 2024

- Savvy DIY Investors Must Plan For Succession - September 4, 2024