Tom Bradley just posted a smart analysis of a new closed-end fund. PIMCO’s newly-launched Global Opportunities Income fund attracted $600 million – the top end of its target. That’s a very warm reception to say the least. I won’t repeat Tom’s excellent analysis but would like to expand on a couple of points he made.

Higher return = higher potential risk

The fund is targeting a distribution equal to 6.5% of the initial value of the fund. The prospectus highlights that the portfolio they’ve designed for this fund boasts a recent yield of 7.2% per year.

With GIC rates and government bond yields so low, too many investors assume that managers like PIMCO – considered an elite bond manager – can achieve high returns without exposing investors to higher risk. As I stated at the MFDA’s Seniors Summit last September – coincidentally on a panel with Tom – investors and advisors must assume that higher potential risk always accompanies the potential for higher returns.

With 7- and 10- year Canada bonds yielding 2% and 2.5% per year respectively anything offering a gross yield north of 7% must – by definition – have significantly higher risk potential than those guaranteed options. The benefits of an offering like this will be obvious but you’ll have to dig a little to uncover the true associated risk factors.

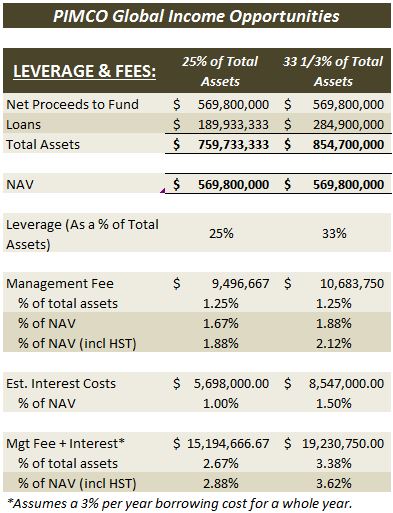

Leverage & fees

Tom notes that the fund’s 1.25% management fee is charged not on the net asset value but on the total – or ‘gross – asset value. For most funds this is little difference between these two descriptions. But it’s an important distinction for a fund employing leverage – i.e. borrowing money to increase total investment assets.

The fund will initially employ leverage equal to 25% of total assets, which equals 1/3rd of the initial net proceeds raised. But management expense ratios are computed on net assets. So charging a 1.25% fee on total assets with 25% leverage equates to a management fee of 1.88% including HST. With its maximum leverage of 1/3, the management fee would be 2.12% including HST on the fund’s NAV.

These figures exclude interest costs from borrowed funds, which could push the fund’s management expense ratio toward 3% annually or higher depending on how much leverage is employed and how long it is maintained.

{kind=link}

IPO investors starting deep in the hole

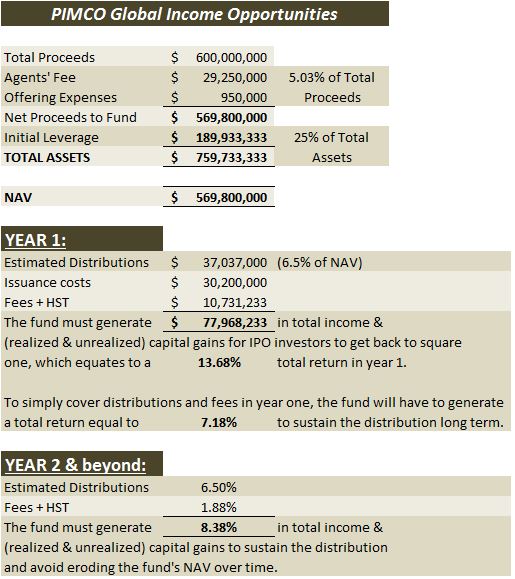

I’m not a fan of buying a closed-end fund at IPO because the most eager investors effectively shoulder all of the costs of listing the fund on the stock exchange. IPO investors ponied up $600 million, out of which they paid $30.2 million in issuance costs. Investors, then, start more than 5% under water out of the gate. Factor in fees and taxes and the fund must generate a total return of 7.2% in year 1 – gross of fees – to get back to square one.

Extending the above calculation, I also find that the fund’s distribution policy – i.e. 6.5% of the initial net proceeds – requires a total return of 13.7% in year one (gross of fees) to cover the issuance costs and the cash distribution. After year one, the fund will need to sustain a minimum total return of 8.4% per year before fees to sustain the distribution longer-term without eroding the unit price.

{kind=link}

While these return thresholds are calculated gross of fees, they don’t take into account the impact of interest costs – which bumps up fees. While the fund’s U.S. cousin – PIMCO Dynamic Income – has generated strong USD returns, this was achieved by taking risk that will materialize the next time credit markets hit a soft patch.

Perhaps this will be a fine investment. But if you invest for yourself or recommend it to clients, make sure you flesh out the above issues and other relevant risks in much greater detail.

- The S&P 500’s Three Surprising Traits - November 6, 2024

- Savvy DIY Investors Must Plan For Succession - September 4, 2024

- The Signs of when to Leave Your Money Manager - May 22, 2024