By Dan Hallett on November 22, 2022

Throughout most of this century, investors have been down on bonds. The argument was that rates are historically low and are bound to rise – which would push bond prices down. (Prior to this year, I’ve heard that my entire career.) With North American bonds having their toughest year ever, I’m here to tell you that bonds remain an important part of investment portfolios. And what about those persistently rising rates that have caused so much trouble all year? They have triggered double-digit losses this year, but higher yields are not so bad longer-term.

Since January 1, 2000, the Canadian bond market has kicked out total returns (before costs, inflation, and taxes) of 4.36% per year through September 2022. If we remove inflation, the tally came to an average annualized return of 2.15%, normal by historical standards.

Bond yields and prices are inversely related. When one goes down, the other goes up (and vice versa) because the coupon – or dollar amount of interest paid to bondholders – is fixed for the life of the bond. The table below shows that Canadian bonds’ yield rose by 2.44 percentage points since the start of this year. That has resulted in a total loss of about -13% so far this year; which hurts in a year when stocks are down significantly.

Note: All statistics calculated from holdings downloaded for the respective dates from https://ca.ishares.com using the iShares Core Canadian Universe Bond Index ETF as a proxy for the Canadian bond market.

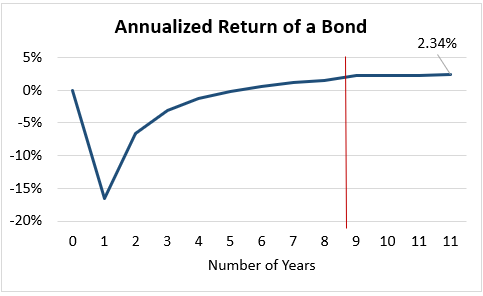

Suppose you purchased bonds at the end of last year – with a term of just over eleven years, a yield to maturity of 1.9%, and a duration of 8.44 years. (Duration is a measure of interest rate sensitivity; the number of years needed to recoup the purchase price of a bond when factoring in the time value of money.) Let’s further assume that in your first year, the yield rises by 2.44 percentage points (as it has this year) and stays constant thereafter. The chart below depicts the journey in terms of a running tally of your annualized total return over the number of years held.

In this example, you end up with a return equal to your starting yield to maturity (1.9%) between years eight and nine. Not coincidentally, that time frame is very close to the duration calculated at the time of your hypothetical purchase (8.44 years). By the end of the term – just over eleven years – you would have an estimated total return of just over 2.3% per year.

If yields don’t change, your next several years will have a higher return – close to the 4.34% per year yield to maturity. While the shorter-term losses are tough to swallow, rising yields result in higher longer-term returns on bonds.

- Piling into U.S. stocks? Don’t Expect the Past Decade to Repeat - January 15, 2025

- The S&P 500’s Three Surprising Traits - November 6, 2024

- Savvy DIY Investors Must Plan For Succession - September 4, 2024