By admin on July 4, 2017

In our quarterly client reports, we use both the MWRR and the TWRR calculations for performance reporting.

First we use the money-weighted methodology to inform clients of the returns that were earned by each of their accounts and their consolidated portfolio.

Then, we show the performance of each of the investments owned within the portfolios using the time-weighted methodology, as this provides a more accurate reflection of how the underlying investment managers performed, excluding the impact of deposit or withdrawal decisions made by the investor.

Our examples below will highlight the differences between TWRR and MWRR:

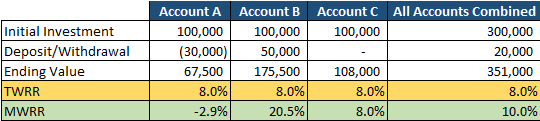

Let’s assume that an investor has three separate investment accounts.

At the beginning of the year, she invests $100,000 into each account and makes the exact same investment in each account. In the first 6 months the underlying investment loses 20% and in the final 6 months of the year the underlying investment rises by 35%.

Let’s also assume that the investor withdraws $30,000 from the first account and deposits $50,000 into the second account immediately after the first 6 months.

The table below provides an example of both the TWRR and the MWRR of each of these three accounts and the total of all three accounts over the 12 month period:

The TWRR is the same regardless of the deposits or withdrawals because it measures the underlying investment’s return.

However the MWRR measures the investor’s performance. Accordingly, MWRR is heavily influenced by the dollar amount and timing of the deposits or withdrawals.

Account B, for example, had a significant deposit right before the investment rebounded – so it had more money benefiting from the rebound. The opposite occurred in Account A. And with no deposits or withdrawals the MWRR for Account C was identical to the TWRR.

When using MWRR, it is much more difficult to compare the performance of various accounts.