Aggressive marketing of investment products is nothing new. Throughout my career I have expended plenty of energy pointing out what I believe to be misleading or overly aggressive marketing initiatives and advertisements. More than four years ago I posted an article highlighting one fund’s sales incentive and another’s misleading benchmark comparison. I have also focused quite a lot of attention on monthly income funds for their aggressive marketing. A few advertisements I’ve seen over the past two weeks quickly grabbed my attention for their questionable claims and content.

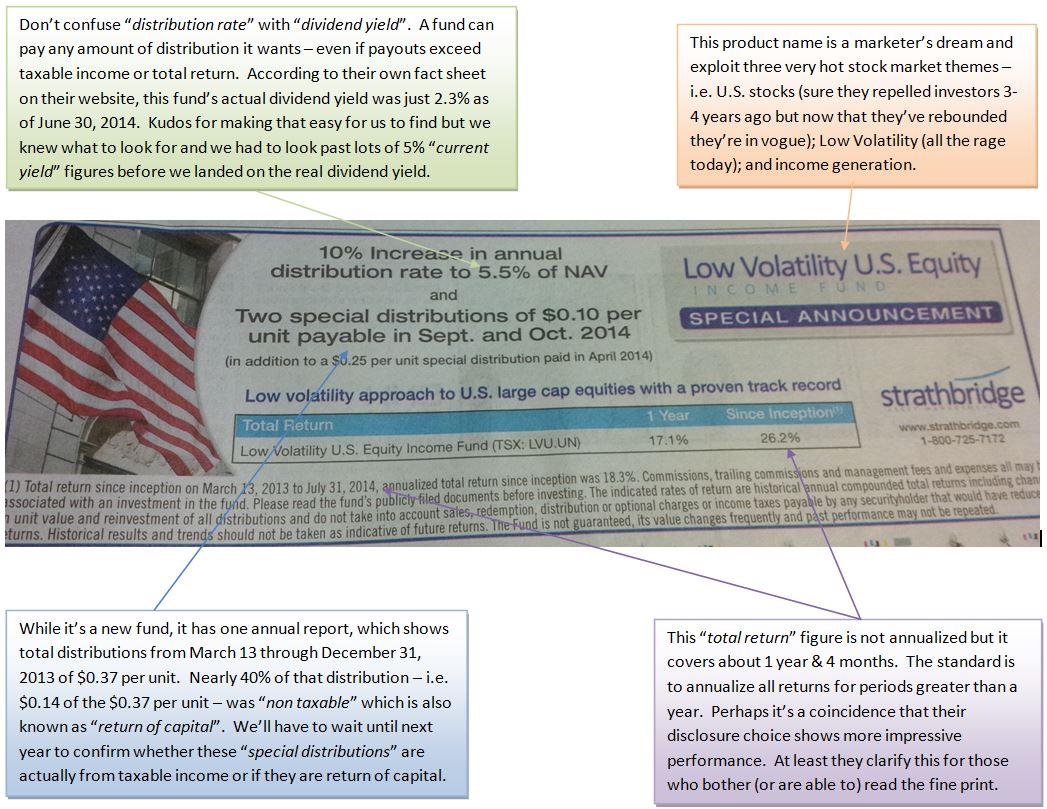

A marketer’s dream fund

I spotted an ad in the Globe & Mail recently for a closed-end fund. It was the name that initially caught my eye for its ability to jump on the bandwagon of a few of today’s hot investment themes. Rather than list my critique here, click on the picture below for the ad with my highlights of things to dig into further if you’re eyeing this fund as a potential investment.

{kind=link}

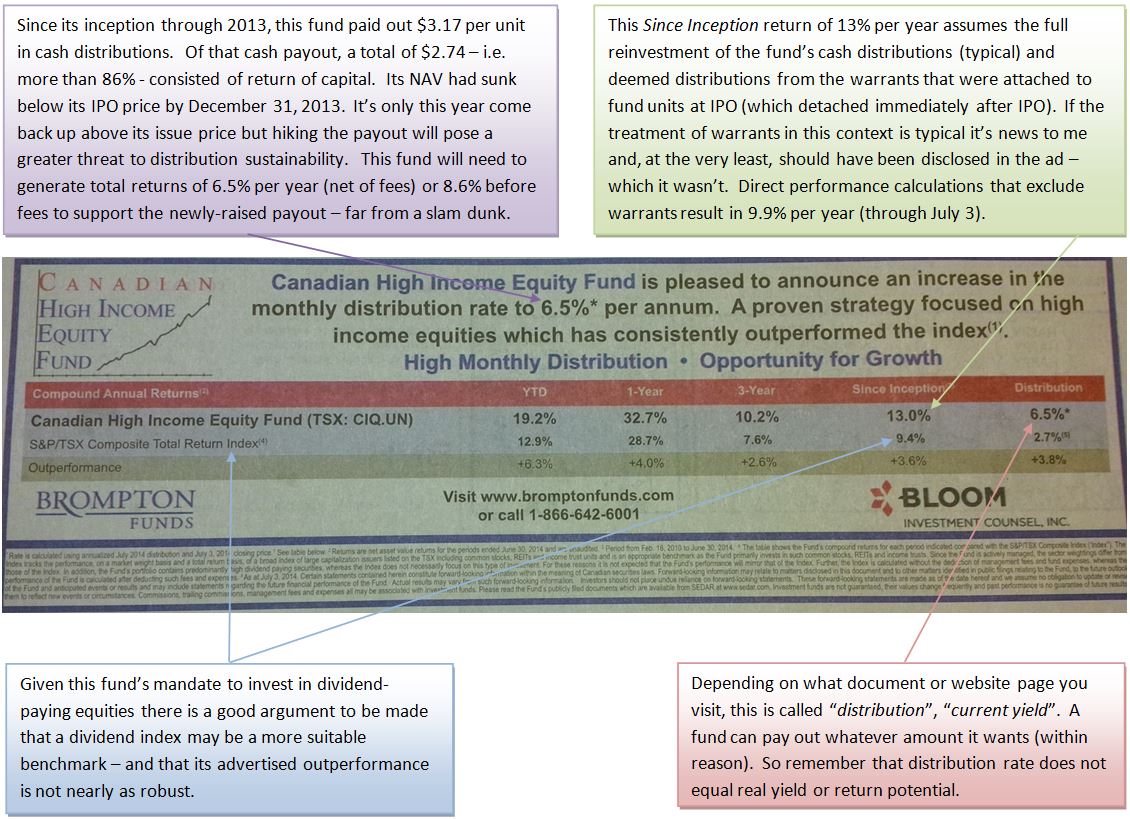

This fund needs to improve its performance disclosure

Credit a claim of fat excess returns and a distribution hike for another recent newspaper ad’s ability to grab my attention. Here is another fund that requires investors and advisors to dig well beneath the surface to understand the basis for the distribution bump and the content of the historical returns. Click below for the ad and my notes.

{kind=link}

Conservative balanced fund benchmarked against the TSX

A couple of weeks ago I also received an email from fund company promoting its conservative balanced fund. The fund’s promotion boasts of its 44% equity upside capture while participating in just 7% of the market’s downside. Before receiving this email I knew nothing about the fund. But I knew that such unusual upside/downside figures signaled that this fund is relatively new and/or that it’s being compared against an inappropriate benchmark.

A little digging revealed both suspicions to be true. The fund has been around for less than three years, meaning that it’s impossible to draw any meaningful conclusions from 32 months of data (through July 2014) in a very rosy environment. My guess that the sponsor based its claim on an unsuitable benchmark also proved true since its upside and downside capture figures were based on a comparison with the S&P/TSX Composite Index.

The email – which was directed at advisors not the investing public – told no lies. But hopefully advisors who received it quickly spotted the inappropriate comparison. A fund with a policy to hold about 1/3rd in stocks should not be compared to a 100% stock benchmark.

At the very least, a fund’s benchmark should reflect its broad asset class policy. In some cases, it can make sense to design a custom strategy-specific benchmark to isolate the manager’s skill. For this income-focused fund, available investment policy details suggest that a benchmark made up of 30% Canadian dividend paying stocks and 70% investment grade Canadian corporate bonds is appropriate.

When comparing the fund against an investable version of this benchmark – using 30% XDV/TSX and 70% XCB/TSX – the fund captured 99% of its benchmark’s upside but 87% of its downside. Overall it has fared well; almost exactly matching its benchmark (both measured net of fees) but it takes on much more credit risk. Perhaps this message doesn’t play well in marketing campaigns:

Capture 99% of the benchmark upside and only 87% of its downside while taking much higher credit risk to just keep up with the benchmark net of fees.

The investment fund business is ultra competitive. Advertisements and marketing material are designed to showcase an investment’s very best attributes. And stretching the truth a bit is legal and par for the course. So take the time before you bite at the next piece of investment marketing bait.

- The S&P 500’s Three Surprising Traits - November 6, 2024

- Savvy DIY Investors Must Plan For Succession - September 4, 2024

- The Signs of when to Leave Your Money Manager - May 22, 2024