By HighView Financial on December 9, 2016

Fee Disclosure Should Just be the Start

Canadian securities regulators are currently forcing fee transparency for client accounts in the investment industry. This change is known as CRM2 (Client Relationship Model, Phase 2). HighView Financial Group has written about CRM2 on many occasions and hosted several educational seminars on this topic for both investors and professionals. We have continuously applauded the securities regulators for finally forcing this change because investors have a right to know, in an easy format, how much they are paying for investment advice.

We have always been fully transparent with our clients – not because we predicted these regulatory changes – but because we believe fee and expense transparency is the right thing to do! It’s about being accountable to your clients. In fact, this is one of our core values.

Although these fee transparency regulatory changes are very positive for Canadian investors, we believe there remains another level of transparency that is still generally avoided in the Canadian Wealth Management industry, and should also be forced by regulators: operational transparency. In other words, in the operation of my portfolio:

- Who are the various service providers?

- Are they professionally competent & proven at providing these services?

- What are they being paid for their services?

- What, if any, conflicts of interest exist amongst these various service providers?

Who Are the Service Providers of My Portfolio?

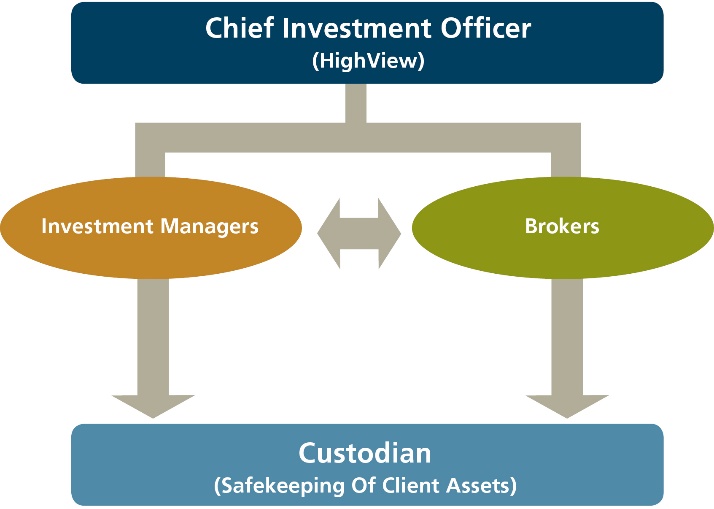

This is my 27th year in the investment industry. Despite the many changes I’ve seen over the past three decades, the core of money management operations (with the exception of significantly increased technology) mostly remains the same. Specifically, in the management of clients’ portfolios, there have been four key participants:

- Advisor: This is the service that relates to the pure advice and counsel with respect to the structuring of an investor’s portfolio aligned against their unique goals, timelines, and tolerances for risk.

- Investment Manager: This is the service that relates to the money management of an investor’s portfolio (i.e. the people who select the stocks and bonds in clients’ portfolios).

- Broker: This is the service associated with the buying & selling of securities (i.e. stocks and bonds) in investor portfolios.

- Custodian: Custody is the service associated with the safekeeping of client assets, independent of any of the other investment providers and service participants.

At HighView, our view has always been that the separation of each of the above activities is paramount in the provision of truly objective and transparent advice and service. We call this the professional division of duties, which is illustrated in the image below:

Why Is Separation Of Professional Duties Important To Investors?

There are three reasons why we believe the separation of these duties is important for investors:

- Professional Competency:

Each participant should be a proven best in class provider of professional services in their area of purported expertise.

2. Conflict Of Interest Elimination:

Each participant should not have control, undue influence, or benefit (directly or indirectly) from the services of another participant.

3. Fair Value Pricing:

Each participant should price their services on the fair price for value delivered in a competitive marketplace.

These principles were at the core of the investment counsel industry when it was founded over 100 years ago, when Arthur M. Clifford started an investment counsel firm in Los Angeles in 1915 (Read about the history of investment counselling). Specifically, in the traditional investment counselling and management industry, there has always been a very clear separation of duties amongst the various professional service participants in order to avoid conflicts of interest and collusion.

Consolidation of Service Providers Creates Transparency Issues for Investors

The Canadian wealth and investment management industries have consolidated over the past three decades due to relaxed regulatory and cross-ownership rules. With this consolidation, the professional separation of duties principle has rapidly deteriorated as large Canadian financial institutions (i.e. banks and insurance companies) have increasingly purchased and/or built all four operational service providers (i.e. advice, investment management, brokerage and custody).

Although these integrated and bundled services (i.e. wrap programs and services) are sold as a convenience for investors, the business logic for this is what our country’s large financial institutions refer to as an ‘increased share of the investor wallet’. In other words, why restrict your services to the provision of only one service when you can offer four services, lock-up the whole client relationship, and make more money!

The ‘wrapping’ or ‘bundling’ of these services into branded ‘investment programs and products’ has become so extreme amongst large Canadian financial institutions that many of their Client-Facing Advisors can no longer tell ‘who’ the various participants are within their clients’ portfolio offerings and ‘how’ the various money management and operational pieces are meant to fit together for the benefit of their clients.

I refer to this approach as ‘wealth bundles’, like Rogers does with your phone, internet, and TV services — but this is with your money! As a result, wealth management amongst Canada’s large financial institutions has become less about living the professional principles the investment counsel industry was founded on, and more about the ‘increased share of investor wallet’ through the branded packaging of integrated investment products and programs.

What’s The HighView Approach?

At HighView, we believe the professional separation of duties, together with full fee and expense transparency, is of paramount importance for both objectivity and transparency. It’s all part of being a true investment fiduciary for our clients, and the reason we have full and complete separation of professional duties of all service provides within our clients’ portfolios.

Our sole source of revenue is the counsel and advice we provide to our clients. All other service providers (i.e. investment managers, brokers, custodians) are completely independent of HighView and are, therefore, only selected for their professional experience and proven competencies, all at institutional pricing levels, and perform their due diligence.

What Should Investors Do When Faced With Transparency Challenges?

If you’re an affluent family client of a wealth management firm that cannot or refuses to unbundle their service providers (together with their respective fees), you must be prepared to ask some tough questions of your wealth management firm with respect to their true investment fiduciary commitments to you.

In other words, are they managing your money to service you, or for the convenience and benefit of themselves? It’s your money and you have the right to expect and demand complete objectivity and transparency of advice, fees, and service of your portfolio!

HighView is an experienced investment counselling firm for affluent Canadian families and foundations. We would be happy to discuss our goals-based investment approach with you and your professional advisors.

Watch our advocacy videos, many of which are about CRM2.

You may also be interested in:

- Investment Industry Participants Finding a Chair before the Music Stops

- Making an Impact: Aligning Values with Investment

- Making Sense of Your New CRM2 Performance Report

- Understanding Wealth Stewardship - August 4, 2022

- Reaching a Successful Transition of Family Wealth - May 12, 2022

- The Obstacles in Creating Sustainable Wealth - April 7, 2022